What is the definition, scope, and significance of the Courier Express and Parcel Market?

The Courier Express and Parcel Market encompasses the industry responsible for the rapid, door-to-door delivery of documents, parcels, and freight across domestic and international networks. Its scope includes B2B, B2C, and C2C shipments across sectors such as retail, manufacturing, BFSI, and agriculture. The market is significant as it underpins global e-commerce, supply chain efficiency, and just-in-time logistics, with a 2026 valuation of 518.73 Billion reflecting its critical economic role.

What are the key drivers, restraints, challenges, and opportunities shaping the Courier Express and Parcel Market?

Key drivers include surging e-commerce adoption, cross-border trade growth, and demand for same-day delivery. Restraints involve high last-mile costs, regulatory complexities, and fuel price volatility. Challenges encompass labor shortages, capacity constraints during peak seasons, and sustainability pressures. Opportunities lie in automation, AI-driven route optimization, green logistics investments, and expanding into underserved rural markets, all supported by a projected CAGR of 9.16%.

What current and emerging trends are influencing the Courier Express and Parcel Market?

Major trends include the rise of omnichannel retailing driving B2C volume, increased use of locker and pickup-point networks, and integration of real-time tracking via IoT. Emerging trends feature drone delivery pilots, autonomous vehicle testing, and blockchain for shipment transparency. Sustainability initiatives such as electric fleets and carbon-neutral shipping are gaining traction, aligning with consumer and regulatory demands across domestic and international segments.

How did COVID-19 impact the Courier Express and Parcel Market and what is the recovery trajectory?

COVID-19 caused an unprecedented surge in parcel volumes as lockdowns accelerated online shopping, straining networks but boosting revenue. The pandemic reshaped consumer expectations for speed and contactless delivery. Recovery has been robust, with volumes stabilizing above pre-pandemic levels. The market is projected to grow from 518.73 Billion in 2026 to 958.11 Billion by 2033, reflecting sustained structural demand shifts.

What does the competitive landscape look like in the Courier Express and Parcel Market?

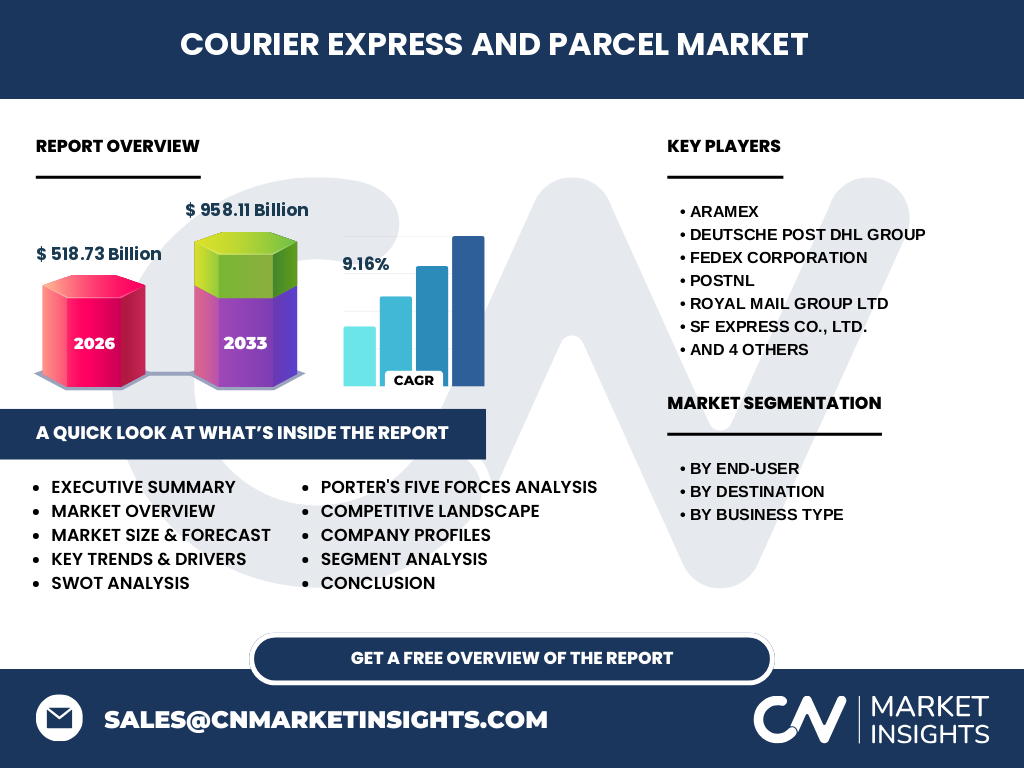

The market is highly consolidated among global integrators and regional leaders. Key players include Aramex, Deutsche Post DHL Group, FedEx Corporation, PostNL, Royal Mail Group Ltd, SF Express Co. Ltd, SG Holdings Co Ltd, Singapore Post Limited, United Parcel Service Inc., and Yamato Holdings Co. Ltd. Competition centers on network density, technology investment, service diversification, and pricing strategies across B2B, B2C, and C2C channels.

What are the key findings and high-level overview from the Executive Summary of the Courier Express and Parcel Market report?

The Executive Summary highlights a market valued at 518.73 Billion in 2026, forecast to reach 958.11 Billion by 2033 at a 9.16% CAGR. Growth is fueled by e-commerce, cross-border trade, and digitalization. Segmentation by end-user (BFSI, retail, manufacturing, agriculture), destination (domestic, international), and business type (B2B, B2C, C2C) reveals diverse revenue streams. Strategic imperatives include last-mile innovation and sustainability.

What are the market projections for the Courier Express and Parcel Market for the 2025-2032 period?

While the provided forecast spans 2027 to 2033, the trajectory indicates strong expansion. The market size of 518.73 Billion in 2026 is expected to nearly double to 958.11 Billion by 2033, representing a 9.16% CAGR. This growth assumes continued e-commerce penetration, infrastructure investment, and recovery from pandemic disruptions, with B2C and international segments leading volume gains.

How is the Courier Express and Parcel Market sized and shared across segmentation categories?

Segmentation analysis breaks the market by end-user into BFSI, retail, manufacturing and construction, and agriculture. By destination, it splits into domestic and international flows. By business type, it covers B2B, B2C, and C2C models. Retail and B2C dominate volume, while B2B contributes high value. International shipments grow faster due to cross-border e-commerce, with each segment offering distinct margin profiles.

What is the geographic distribution of the Global Courier Express and Parcel Market by region?

The report provides a detailed geographic breakdown of market size and share across major regions, analyzing performance in North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Regional dynamics vary by e-commerce maturity, infrastructure quality, and regulatory environment, with Asia-Pacific showing the fastest growth driven by China and India.

What does the detailed regional analysis reveal about the Courier Express and Parcel Market performance?

Regional analysis examines market size, growth rates, competitive intensity, and key trends per geography. North America and Europe lead in per-capita spend and technology adoption. Asia-Pacific dominates volume growth due to massive e-commerce ecosystems. Latin America and MEA present emerging opportunities with improving logistics infrastructure. Each region's domestic versus international split and B2B/B2C mix are quantified.

Who are the leading companies in the Courier Express and Parcel Market and what are their strategies?

Leading companies profiled include Aramex, Deutsche Post DHL Group, FedEx Corporation, PostNL, Royal Mail Group Ltd, SF Express Co. Ltd, SG Holdings Co Ltd, Singapore Post Limited, United Parcel Service Inc., and Yamato Holdings Co. Ltd. Strategies focus on network expansion, digital platforms, sustainability commitments, M&A for geographic reach, and specialized solutions for healthcare, cold chain, and high-value goods.

What does Porter's Five Forces Analysis indicate for the Courier Express and Parcel Market?

Porter's Five Forces reveals high competitive rivalry among established integrators. Threat of new entrants is moderate due to high capital requirements but lowered by digital platforms. Buyer power is strong with large e-commerce clients negotiating rates. Supplier power (fuel, labor, vehicles) is significant. Threat of substitutes is low for time-sensitive shipments but rises with digital document transfer.

What are the strengths, weaknesses, opportunities, and threats in the SWOT Analysis of the Courier Express and Parcel Market?

Strengths: essential service, global networks, technology assets. Weaknesses: high fixed costs, labor dependency, carbon footprint. Opportunities: e-commerce growth, automation, green logistics, emerging markets. Threats: economic downturns, regulatory changes, fuel volatility, disruption from crowdsourced delivery models. The 9.16% CAGR underscores opportunity outweighing threats.

How does the Value Chain Analysis describe the Courier Express and Parcel Market structure and value flow?

The value chain spans pickup, sorting, line-haul transport, customs clearance, last-mile delivery, and returns management. Value accrues at each stage through technology-enabled visibility, density optimization, and service differentiation. Upstream includes fleet and facility investment; downstream focuses on customer experience. Integration across the chain via digital platforms enhances margin capture for integrated players versus pure last-mile operators.

What are the key investment insights and strategic recommendations for the Courier Express and Parcel Market?

Investment insights highlight last-mile automation, electric vehicle fleets, AI-driven demand forecasting, and cross-border e-commerce enablement as high-return areas. Strategic recommendations include acquiring regional specialists, building open logistics ecosystems, investing in sustainable packaging, and developing data monetization services. The forecasted growth to 958.11 Billion by 2033 supports capital allocation toward capacity and technology.

What are the summary conclusions and key takeaways for the Courier Express and Parcel Market?

The market is on a strong growth trajectory, driven by structural shifts in commerce and supply chains. With a 2026 base of 518.73 Billion and a 9.16% CAGR to 958.11 Billion by 2033, the sector offers substantial opportunities. Success requires balancing cost efficiency with speed, sustainability, and digital customer experience across B2B, B2C, and C2C segments globally.

What research methodology was used to conduct this Courier Express and Parcel Market study?

The research employs a combined primary and secondary approach. Primary research includes interviews with industry executives, carrier representatives, and e-commerce shippers. Secondary sources encompass company filings, trade associations, government statistics, and proprietary databases. Market sizing uses bottom-up and top-down validation, with segmentation cross-checked against revenue disclosures from key players like FedEx, UPS, and DHL.

What is the research scope and coverage limitations for the Courier Express and Parcel Market report?

The scope covers market size, segmentation, competitive landscape, regional analysis, and forecasts from 2025-2032. It includes all major courier, express, and parcel services across B2B, B2C, and C2C. Coverage excludes freight forwarding, traditional postal mail, and specialized heavy freight. The report focuses on commercial carriers and integrators, with financial figures based on the provided 2026 and 2027-2033 data points.

Which key companies are featured and what recent developments have they announced in the Courier Express and Parcel Market?

Key companies include Aramex, Deutsche Post DHL Group, FedEx Corporation, PostNL, Royal Mail Group Ltd, SF Express Co. Ltd, SG Holdings Co Ltd, Singapore Post Limited, United Parcel Service Inc., and Yamato Holdings Co. Ltd. Recent developments encompass network expansions in Asia, sustainability-linked financing, autonomous delivery pilots, strategic partnerships with e-commerce platforms, and acquisitions strengthening cross-border capabilities, reflecting dynamic competitive positioning.